ChatGPT has introduced an AI financial management feature for its Pro users, allowing direct connections to financial accounts to generate financial dashboards and provide spending advice based on real data. However, contrary to expectations, overseas users have largely rejected this new feature.

The Challenge of Trust in AI Finance

The biggest hurdle for AI finance has never been technology, but user trust, which is vividly illustrated in this case. Why is there no skepticism when AI is embedded in native financial apps, but a universal model connecting to finance triggers collective resistance? Let’s analyze this from a different angle.

OpenAI’s announcement screenshot showcasing the financial management feature for ChatGPT Pro users.

AI Moves from Content Generation to Financial Management

OpenAI’s launch of the AI financial management feature has been in the works for some time. In April of this year, it acquired the team from personal finance startup Hiro, whose founder, Ethan Bloch, and ten core members joined OpenAI. Hiro previously helped users manage over 6.8 billion yuan in assets as a “personal CFO” using AI.

This is not a spontaneous attempt by OpenAI but a collective choice in the AI industry. In the same week, ByteDance’s Doubao app launched a QR code payment feature, leveraging Douyin Pay to create a closed-loop from AI dialogue to shopping to payment, directly extending AI from a conversational tool to consumption scenarios.

Domestic financial giants have been ahead in this regard. Alipay launched its AI financial assistant “Zhixiaobao” back in 2024, followed by a complete upgrade of Ant Group’s AI model-driven “Mxiaocai,” which provides users with market analysis, portfolio insights, and educational support, covering over 1 billion monthly active users.

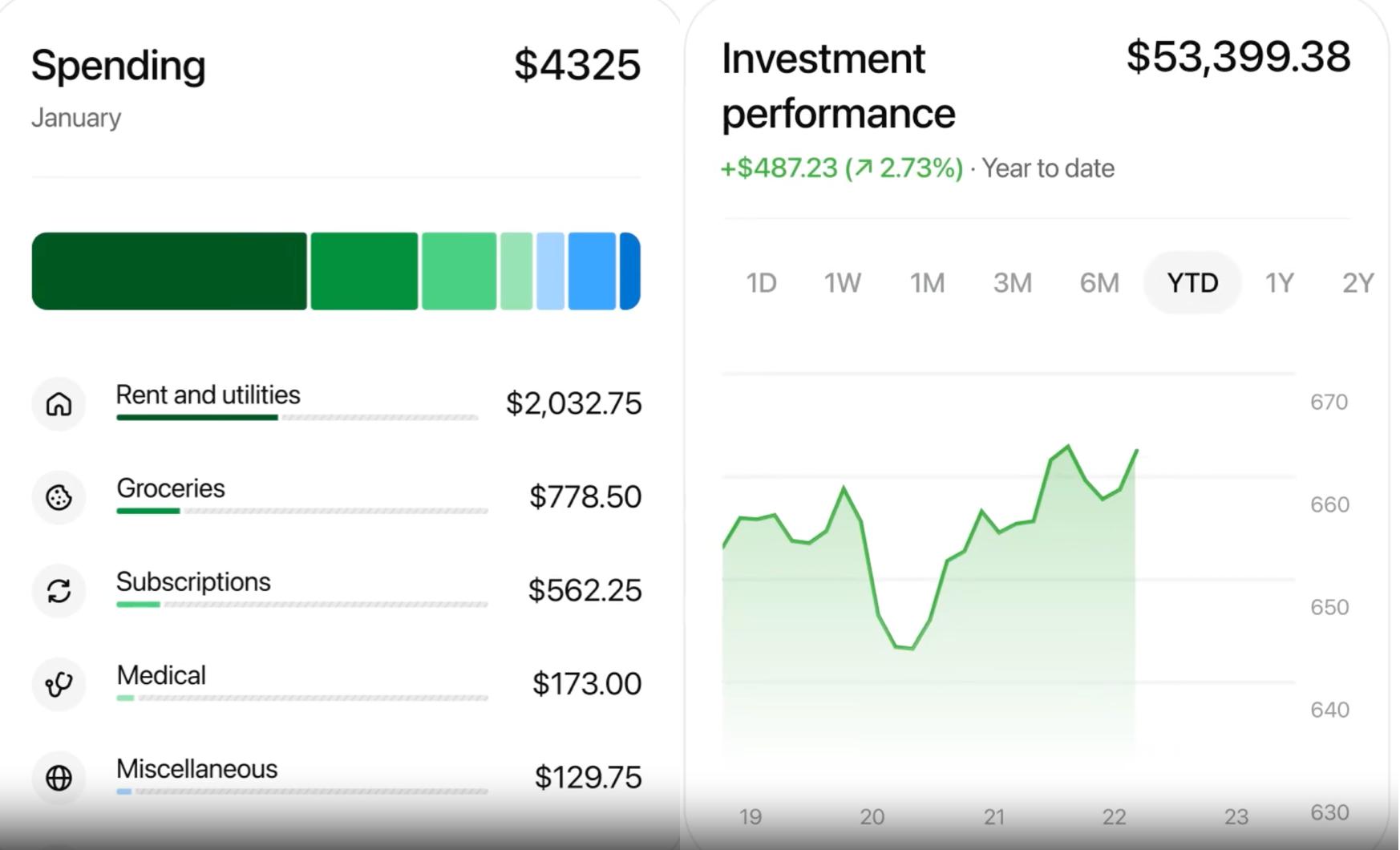

Screenshot of ChatGPT’s financial data dashboard showing expenditure details and investment returns.

Market signals are also clear. According to data cited by Investor Network, the global AI-driven smart investment advisory market is expected to grow from $6.6 billion in 2025 to $9.77 billion in 2026, with a compound annual growth rate of 47.9%.

This growth hides a key change: AI has officially moved from “content generation” to “decision support” in deep scenarios, with financial decision-making being the most sensitive and demanding type of decision.

Younger users are actually ready for this. Research shows that 41% of Gen Z investors are willing to trust AI to manage their portfolios, and 67% of Gen Z traders have activated AI tools in their daily trading. Demand is rising, so why did ChatGPT’s new feature fail?

User Rejection: Not AI Finance, But Data Leakage

OpenAI has implemented rules, clarifying that ChatGPT only has “read-only access” to financial accounts and cannot move user funds. Users can disconnect at any time, and synchronized data will be deleted within 30 days. The privacy chat mode does not use any financial data.

However, users remain unconvinced, with comments on X overwhelmingly negative: “It’s crazy to hand over financial privacy to AI,” and “The word privacy is disappearing.” Some users worry that AI might secretly subscribe them to unnecessary services. Digital Trends directly stated, “I won’t connect.”

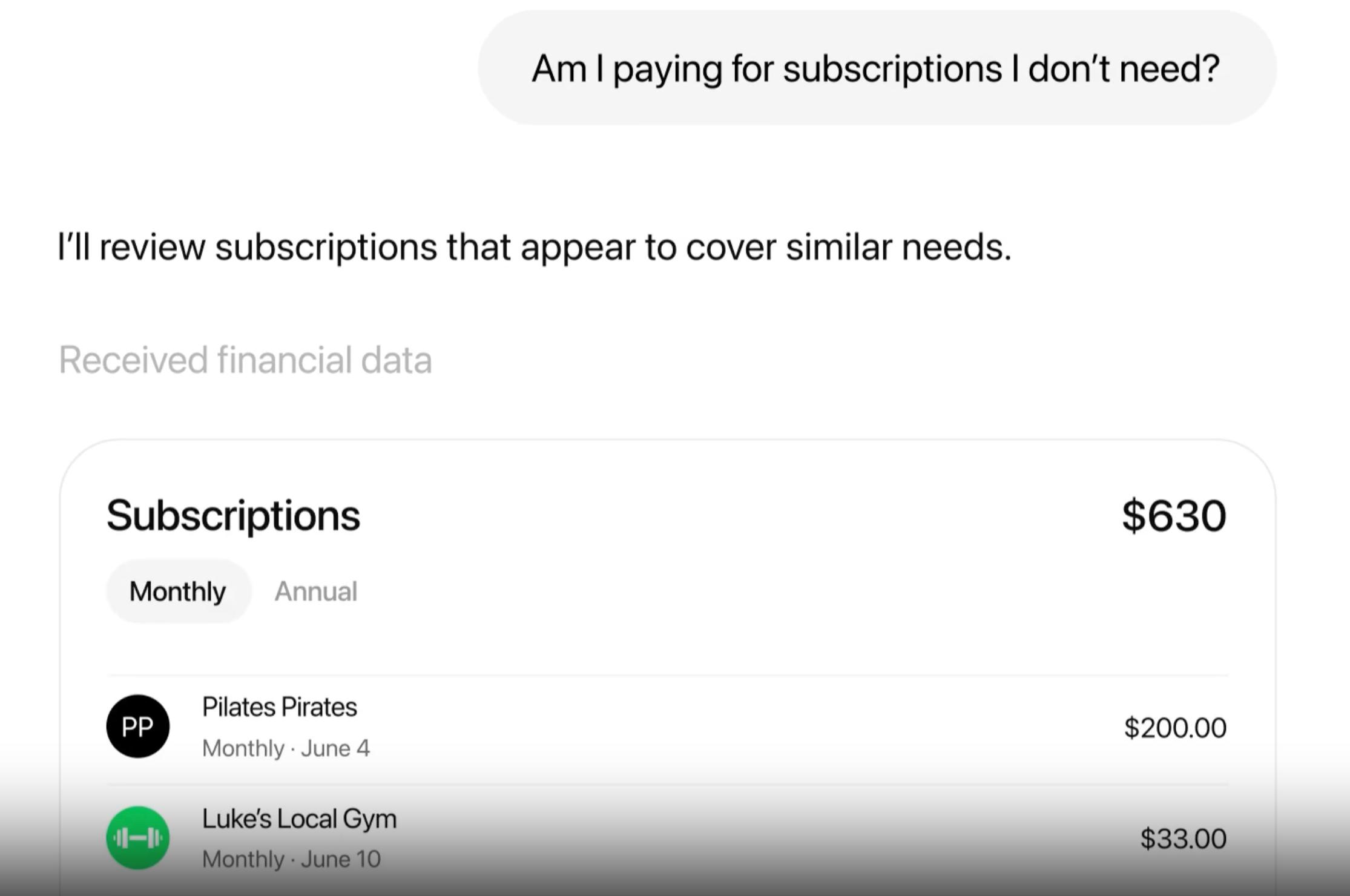

Screenshot of ChatGPT’s subscription fee inquiry interface showing monthly subscription items and total costs.

Why do users have such different attitudes toward AI finance on different platforms? Domestic users have never raised privacy concerns using Alipay’s Mxiaocai, while ChatGPT’s launch sparked outrage. The core difference lies not in technology but in data boundaries.

What users truly worry about is not the right to delete data, but how many third parties have access to their data during storage and analysis. General AI platforms do not hold financial licenses and are not subject to financial-grade data regulations, meaning that core financial data routed through Plaid to a general model is akin to placing their most private information on non-financial institution servers.

Screenshot of Alipay’s AI financial assistant interface showing the function entry and data.

The logic of native financial apps is completely different. Users’ payment, investment, and debt data already reside within the platform, which holds compliance licenses and has been subject to financial-grade security regulations since day one. The data boundary has never changed.

Ant Group’s Mxiaocai is a prime example: AI capabilities are simply added on top of the existing security framework, and data has never left Alipay’s secure boundary. Users do not need to share any new private information, naturally avoiding a trust crisis.

Screenshot of Alipay’s Mxiaocai interface showing Mxiaocai’s financial Q&A and analysis features.

Interestingly, ChatGPT’s disclaimer states, “Your complete financial situation is within ChatGPT,” but the fine print at the end clarifies: “ChatGPT is not a substitute for professional financial advice.”

Screenshot of ChatGPT’s disclaimer showing that ChatGPT does not provide professional financial advice.

OpenAI updated its usage policy by the end of 2025, explicitly prohibiting ChatGPT from providing financial, legal, or medical advice, having previously received subpoenas due to user losses caused by AI advice. The simultaneous launch of financial features while distancing itself from responsibility highlights an inherent issue.

The True Breakthrough for AI Finance Lies Beyond General Models

Many interpret this controversy as a sign of user distrust in AI finance, but this is entirely incorrect. Users are not rejecting AI managing their finances; they are rejecting the general model extracting their core financial data from outside.

This incident actually confirms an overlooked trend: the core barrier for financial AI has never been the general capabilities of large models, but the legally held data and compliant security frameworks. This is precisely the greatest advantage of native financial institutions and the barrier that general AI platforms find hard to cross.

From a technical perspective, general models can indeed provide more humanized analysis than traditional tools and can help users sort through chaotic cash flows to identify unnecessary subscription expenses. For instance, ChatGPT’s showcased feature can automatically organize all user subscriptions, calculate monthly total expenses, and help users identify idle subscriptions with one click.

Screenshot of overseas users’ comments expressing skepticism about ChatGPT’s financial feature.

This feature is inherently valuable to users, but the problem lies in the implementation path: must data be exported to a general model for analysis? Native financial apps can integrate the same AI capabilities within their local data framework, allowing users to enjoy AI benefits without incurring additional privacy risks.

The future evolution of AI finance is already clear from this controversy: it is not about general AI forcibly invading the financial sector, but rather native financial institutions upgrading their service capabilities with AI. This is akin to adding a new weapon to an already fortified castle, allowing users to benefit from AI without opening the door to their data.

The industry already has a clear hierarchy of players:

- Licensed financial institutions: Hold data and compliance advantages, only needing to add AI capabilities for rapid implementation, resulting in almost zero trust costs.

- Native financial super apps: Integrating data, users, and compliance, this is the fastest-growing sector for AI finance.

- General AI platforms: Can only output tools under data desensitization, making it difficult to touch core financial data.

Gen Z’s acceptance of AI finance is already high, and the demand explosion is on the way. However, the competition on the supply side has always been a competition of rules and trust, rather than a simple competition of model capabilities.

Model capabilities can catch up quickly, but the barriers of trust and compliance require long-term accumulation and cannot be broken by a single feature release.

ChatGPT’s misstep serves as a reminder to all players: in the unique field of finance, technology can solve only half the problems; the other half will always be trust and rules. Skipping trust to discuss functionality will lead to users voting with their feet.

AI must respect the rules of money to get close to it. Data has boundaries, and trust will have space only when those boundaries are respected. This principle applies equally to both general AI and financial AI.

Comments

Discussion is powered by Giscus (GitHub Discussions). Add

repo,repoID,category, andcategoryIDunder[params.comments.giscus]inhugo.tomlusing the values from the Giscus setup tool.